Want one of these for the company you're actually watching?

Free first thesis. No card. Thirty minutes from ticker to inbox.

At what price would the agents act?

Full thesis

Tesla, Inc. (TSLA) — Investment Thesis

2026-05-26

Summary

| Metric | Value |

|---|---|

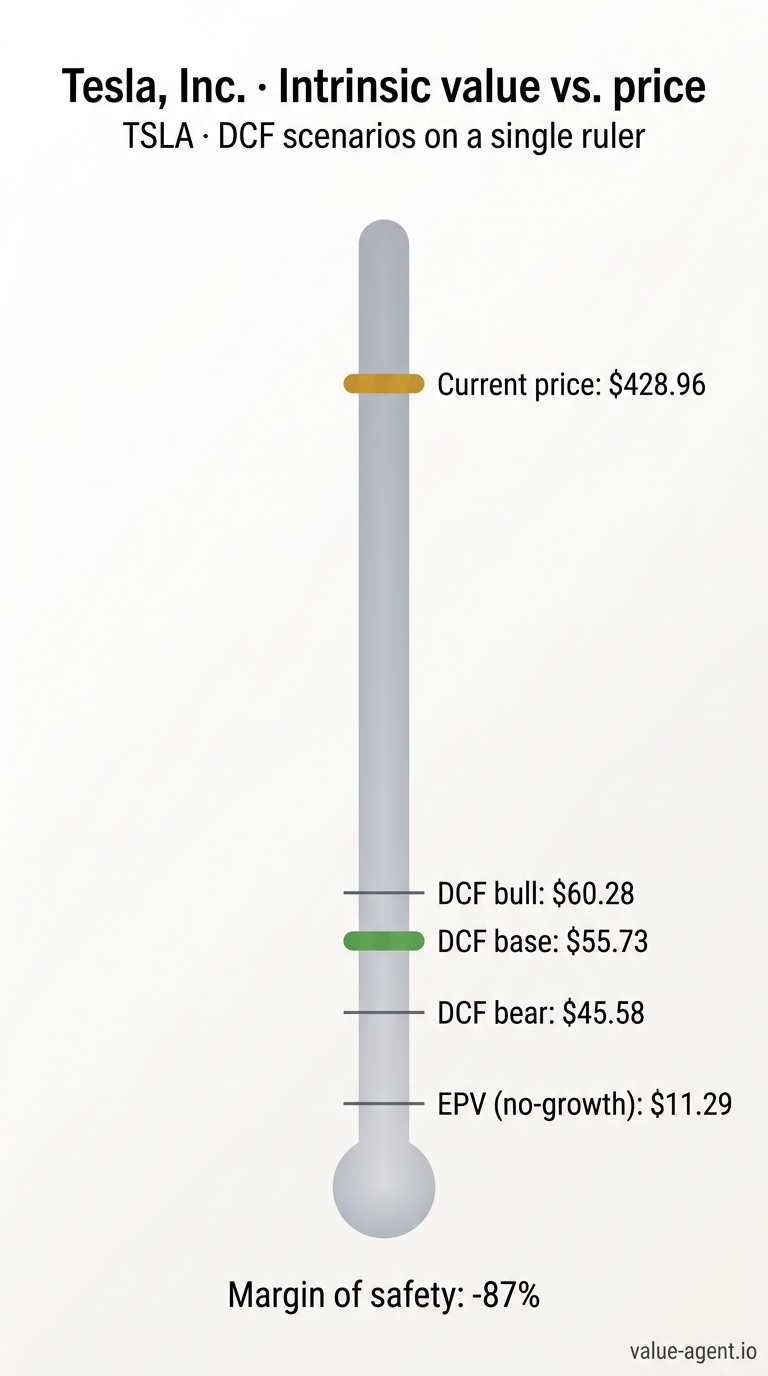

| Verdict | Avoid · high conviction · Quality 3/10 |

| Current price | $428.96 |

| IV (DCF Bear / Base / Bull) | $ 45.58 / $ 55.73 / $ 60.28 |

| IV (EPV) | $11.29 |

| Margin of Safety @ Base | -669.8% |

| Reverse-DCF implied growth | +50.0% |

| Latest FCF | $6,220 M |

| FCF 5yr CAGR | +17.4% |

| Revenue 5yr CAGR | +24.6% |

| Latest ROIC | 4.8% |

| ROIC 10yr avg | -10.8% |

| Macro | CAPE 42.0 · 10Y 4.57% · Buffett indicator 229.6% |

| Management Credibility | D |

(All values from the canonical verdict object and pre‑computed metrics, with n/a for unavailable items.)

The Business in One Paragraph

Tesla designs, manufactures, and sells electric vehicles (Model 3, Y, S, X, Cybertruck, Semi), energy storage and solar systems, and is pushing into AI‑driven autonomous driving and robotics. The automotive segment—which accounts for the overwhelming bulk of $94,827 M in FY2025 revenue [dp]—sells directly to consumers, while the energy business deploys grid‑scale batteries and solar products. The stock’s current narrative, however, hinges on speculative ventures: the Robotaxi ride‑hailing service launched in June 2025 [10K‑BIZ‑2026‑p1], Full Self‑Driving (FSD) software, and the Optimus humanoid robot, none of which yet generate material disclosed revenue. Our circle‑of‑competence pre‑screen flagged Tesla as not understandable precisely because its valuation rests on these early‑stage, binary‑outcome bets with unpredictable economics.

Financial Analyst Deep Dive

(The following is the full Financial Analyst Report — reproduced verbatim as sourced.)

Financial Analyst Report — Tesla, Inc. (TSLA)

Date: 2026-05-26 | Price: $428.96 | Market Cap: $1.61T | Rating: AVOID

The 10-Year Story in One Paragraph

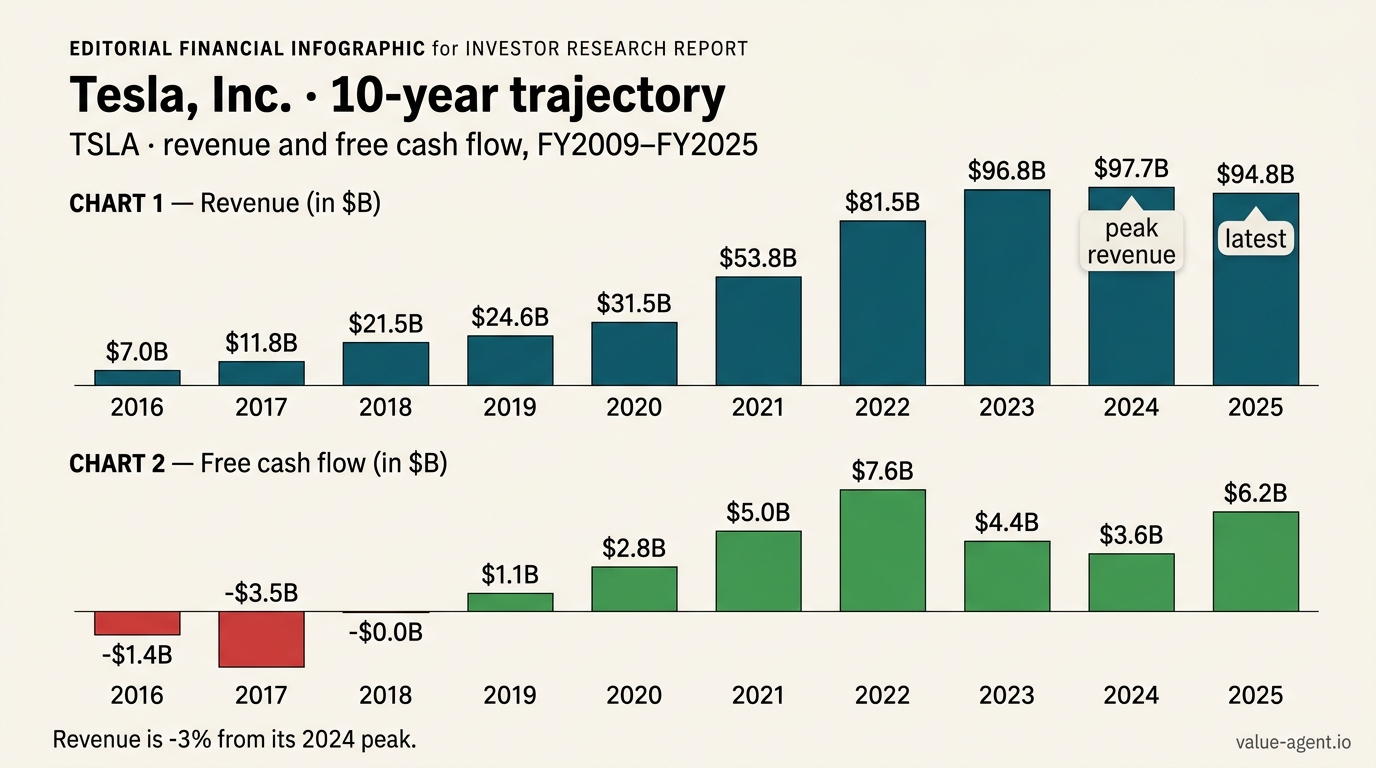

Tesla's numbers tell a story of two completely different businesses. From 2016–2022, it was a genuine industrial miracle: revenue compounded at 37.1% annually [pc], operating margins hit 16.8%, and ROIC peaked at 36.6% [pc] — figures that would make any Buffett-style analyst take notice. But since FY2022, the core automotive franchise has been in accelerating structural decline: 3-year revenue CAGR of just +5.2%, operating income CAGR of –31.7%, and ROIC that has collapsed from 36.6% to 4.8% over three consecutive years [pc]. The stock at $428.96, however, is priced as though the miracle never ended. Our DCF base case yields an intrinsic value of $55.73 per share — a margin of safety of –669.8% [pc]. The reverse-DCF implied growth rate is +50.0%, at the absolute ceiling of our model. The market is implying +50%+ growth, beyond what any reasonable DCF can support — this is the strongest signal of overvaluation our framework can produce. Tesla is not just overvalued; it is off the scale.

Top-Line Trajectory

The revenue arc is a textbook S-curve that has flattened. After the explosive run from $7,000M (2016) to $81,462M (2022) — a span during which YoY growth exceeded 50% in four separate years [pc] — the top line has decelerated with brutal consistency: +18.8% in 2023, +0.9% in 2024, and –2.9% in 2025 [pc]. The 3-year revenue CAGR now stands at just +5.2%, a dramatic compression from the 5-year CAGR of +24.6% [pc].

FY2025 was the first revenue contraction year since the Model 3 ramp era: $94,827M, down from $97,690M [dp]. Vehicle deliveries fell to approximately 1.64 million units from ~1.79 million [10k-mda-2026-p1]. This is not a soft patch — it's a directional break. Revenue inflections tell the same story: the last three years have all been negative inflections (deceleration events), the most recent being the –17.8pp drop from 2023 to 2024 [pc].

The quarterly data reinforces the concern. Peak-quarter (Q3) revenue declined from $71.98B in 2024 to $69.93B in 2025 [quarterly]. The TTM revenue of $153,479M shows a YoY decline of –27.5% versus the prior TTM [pc]. While Q1 2026 revenue of $22.39B showed +15.8% YoY growth from Q1 2025, this is off a deeply depressed base and remains well below prior peak levels [quarterly].

The energy storage business is the one bright spot: deployments surged from 31.4 GWh in 2024 to 46.7 GWh in 2025 (+49%) [10k-mda-2026-p1]. But this segment — while growing — is not large enough to offset the automotive decline, and management itself warns that "the current tariff regime will have a relatively larger impact on our energy generation and storage business" [10k-mda-2026-p1].

Profitability Evolution

Operating margin has been on a relentless downward march: 16.8% (2022) → 9.2% (2023) → 7.2% (2024) → 4.6% (2025) [pc]. That is a 12.2-percentage-point erosion in three years. Each year since FY2022 has registered as a margin inflection event (>5pp change) [pc].

Operating income has fallen from $13,656M (2022) to $4,355M (2025) — a 68.1% decline over three years [dp]. The 3-year operating income CAGR is –31.7% [pc]. The compounding direction here is not ambiguous; it is accelerating downward. YoY operating income growth: –34.9% (2023), –20.4% (2024), –38.5% (2025) [pc].

What's driving this? Management's narrative repeatedly cites "cost reduction efforts" and "operational efficiencies," but the numbers show price cuts overwhelming any cost savings. The strategy of "increasing affordability" — management's preferred euphemism [cred] — has meant slashing vehicle prices to sustain volumes, and the cost structure has not kept pace. Net income, which hit a misleading record of $14,997M in 2023 due to a $5.93B one-time non-cash tax benefit, fell to $7,091M in 2024 and $3,794M in 2025 [dp]. Strip out the tax benefit, and the underlying earnings trajectory is even worse than the headline 3-year net income CAGR of –32.9% [pc] suggests.

At 4.6%, Tesla's operating margin now sits below that of well-run traditional automakers — a stunning reversal for a company that once claimed structurally superior margins. This is not a cyclical dip; it is a competitive normalization.

Returns on Capital

ROIC is the single most damning number in this dataset. The trajectory: 36.6% (2022) → 14.4% (2023) → 9.0% (2024) → 4.8% (2025) [pc]. That is four consecutive annual declines, with the auto-detected red flag explicitly calling this a "moat erosion signal" [pc].

Think about what 4.8% ROIC means. At a 10-year Treasury of 4.57% [macro], Tesla's return on invested capital barely exceeds the risk-free rate. This from a company that posted 30.6% in FY2021 and 36.6% in FY2022 [pc]. The business earned those returns for exactly two years — FY2021 and FY2022 are the only years ROIC exceeded 15% [pc]. The median ROIC over the full 10-year window is –1.84% [pc]. The high-ROIC years look increasingly like an anomaly driven by a unique confluence of limited competition, pent-up EV demand, and pandemic-era supply constraints that allowed premium pricing.

The capex narrative makes this worse. Tesla spent $11,342M on capex in FY2024 [dp] — its highest ever — only to produce revenue growth of 0.9% and an operating income decline of 20.4%. Then in FY2025, capex was slashed to $8,527M [dp], a 24.8% cut, and the FCF surge that followed (to $6,220M) was entirely capex-driven, not operations-driven. Capex/D&A ratio has averaged 3.57x [pc], indicating heavy growth investment relative to asset consumption — yet that investment is yielding diminishing, then negative, marginal returns.

When a business spends heavily and ROIC goes down, it means the incremental invested capital is earning below the cost of capital. When it then cuts spending and ROIC still goes down, it means the existing capital base is also deteriorating. This is the classic pattern of a moat in retreat.

Cash Flow Quality

The cash conversion story is superficially strong. FCF/NI conversion ratio averages 1.30x, with a median of 0.76x [pc]. Operating cash flow exceeded net income in seven of the last eight quarters [quarterly]. The Piotroski F-Score sits at 6/9, and the Sloan accruals ratio of –8.4% is well within normal range [pc]. The accounting, by these forensic gates, appears clean.

But these headline figures are deeply misleading for an equity holder, because of one overwhelming factor: stock-based compensation. SBC has averaged 50.2% of reported FCF over the period [pc]. This means that for every dollar of "free cash flow" the company reports, roughly fifty cents is quietly transferred from shareholders to employees and executives — not in cash, but in ownership dilution. True FCF after SBC over the last five years: $2,894M (2021), $6,006M (2022), $2,545M (2023), $1,582M (2024), $3,395M (2025) [pc].

Notice FY2025: reported FCF of $6,220M looks healthy. True FCF after SBC is $3,395M — barely half. And this is in a year when capex was cut dramatically to juice the FCF number. In FY2024, true FCF after SBC was a mere $1,582M against a market cap that now stands at $1.61 trillion.

The cash conversion cycle has also deteriorated. It moved from –26 days in 2021 (Tesla was effectively being financed by its suppliers and customers) to +13 days in 2025 [pc]. Days payable outstanding compressed from 91 days (2021) to 63 days (2025), while days sales outstanding ticked up from 13 to 18 days [pc]. The negative CCC was a genuine competitive advantage — suppliers granting Tesla generous terms. That advantage is shrinking.

Capital Allocation Grade (A–F)

Grade: D

Tesla's capital allocation record is poor on every dimension that matters to outside shareholders.

Buybacks vs. dilution: There have been zero share repurchases across the entire period [er]. Meanwhile, shares outstanding have increased by +30.31% over the last 5 years and +89.44% over the last 10 years [pc]. This is not a split artifact — it is genuine dilution from equity compensation. The $23.7 billion "2025 CEO Interim Award" of 96 million restricted shares [er] sits on top of the still-contested 2018 option award. When (not if) these vest, the dilution cascade will be extreme. No expense is being recognized today, creating the risk of a sudden multi-billion-dollar catch-up charge [er].

Dividends: None. Ever.

M&A track record: Zero acquisitions across five fiscal years [er]. For a large-cap company in an industry undergoing consolidation and technological transformation, the complete absence of M&A is an extreme outlier. It suggests an insular culture unwilling or unable to use its richly-valued equity as acquisition currency.

Capex discipline: The capex/D&A ratio of 3.57x [pc] indicates heavy investment, but as demonstrated above, the returns on that investment are collapsing. In FY2025, capex was cut 24.8% to engineer a FCF recovery — a move that raises questions about whether prior spending was wasteful or the growth pipeline has been abandoned.

Liquidity management: The $5.0 billion unsecured revolver established in 2023 remains undrawn [er]. Cash and equivalents stand at $16,513M [dp]. The balance sheet is liquid. But liquidity without returns is just capital waiting to be diluted away.

The only reason this is not an F is the debt management: total debt was reduced to just $1,029M by 2022 [dp] before creeping back up. But at 8.0% debt/equity in 2025 [pc], leverage is not the problem. The problem is that all shareholder value creation flows to management, not shareholders.

Balance Sheet Strength

Tesla's balance sheet is genuinely strong — and that's the tragedy. Net debt is deeply negative at –$9,929M in 2025 [pc], meaning cash and equivalents of $16,513M [dp] exceed total debt of $6,584M [dp]. Debt/Equity is just 8.0% [pc]. The company ended FY2025 with $44.06 billion in cash, cash equivalents, and investments — a figure from the balance sheet, though not directly quoted in the supplied MD&A excerpt [10k-mda-2026-p1]. The $5.0 billion revolver is undrawn [er]. This is a fortress balance sheet.

But the trend bears watching. Total debt has risen from $1,029M (2022) to $6,584M (2025) — a 540% increase in three years [dp]. The 5-year debt change is –22.19%, but that reflects the 2022 trough; debt has been growing since [pc]. Meanwhile, the debt/equity ratio moved from 2.3% (2022) to 8.0% (2025) [pc].

The balance sheet strength raises a pointed question: with $44 billion in liquidity, why is the company issuing massive equity awards to the CEO rather than buying back stock? Why is there no dividend? The capital is there. The willingness to return it to shareholders is not.

Tellingly, the Corporate Events report flags that Tesla's governance has progressively tightened: a jury trial waiver for "internal entity claims," a 3% ownership threshold to bring derivative suits, and uniform indemnification agreements for all directors and officers [er]. These are the moves of a board insulating itself, not one aligned with shareholders.

Red Flags & Accounting Concerns

1. ROIC declining for 3+ consecutive years (moat erosion signal) [pc]. This is the most important red flag and it is not a false positive. ROIC has fallen from 36.6% to 4.8% over four years across two very different capex regimes (high spend in 2023–2024, low spend in 2025). The decline is structural, not cyclical.

2. Share-count dilution of +30.31% over 5 years [pc]. This flag is real and material. It means per-share intrinsic value is meaningfully lower than aggregate company value suggests. The $23.7 billion CEO interim award is not yet reflected in dilution but will be.

3. SBC averages 50.2% of reported FCF [pc]. This flag is accurate and damning. True free cash flow available to equity holders is roughly half what the headline suggests. In a DCF valuation, using reported FCF without adjusting for SBC systematically overstates intrinsic value.

4. Latest quarter YoY –68.9%, 93.5pp below 5-year CAGR [pc]. This flag requires context. The quarterly data shows Q1 is seasonally low and the most recent quarter (Q1 2026) actually showed +15.8% YoY revenue growth [quarterly]. The –68.9% figure appears to reflect a specific comparison point. However, the TTM revenue decline of –27.5% [pc] confirms the broader deceleration signal is directionally correct.

5. Debt grew +9,066% over the full period [pc]. This flag is a statistical artifact of the near-zero debt base in some years. As noted above, current debt of $6,584M against $16.5B in cash is not a solvency concern. I would discount this flag.

Additional flags I would add:

6. The FCF illusion in FY2025. FCF rose 73.7% YoY [pc] not because the business improved but because capex was cut by $2,815M — more than the entire decline in operating cash flow [dp]. The specialist report correctly calls this "a value mirage" [specialist-fy2025].

7. Warranty reserve risk. The auditor's critical audit matter specifically flags the $8,607M automotive warranty reserve as requiring "significant judgment" and "especially challenging, subjective, or complex judgments" [10k-fs-2026-p1]. The auditors brought in independent specialists to evaluate management's assumptions. This does not mean the reserve is wrong, but it means the number is highly judgment-dependent and could move materially.

8. The deferred compensation time bomb. The 2025 CEO Performance Award's expense recognition is deferred until "the performance condition becomes probable" [er]. When that happens, a multi-billion-dollar charge will hit the income statement in a single period. The market appears to be ignoring this.

Management's Track Record

The Management Credibility Report assigns a grade of D with a net assessment of EVASIVE [cred]. The findings are devastating and I endorse them fully.

Across three year-to-year transitions, management has kept 7 promises, partially kept 1, broken 7, and left 3 unverifiable [cred]. The kept promises cluster around product launches (Cybertruck, Tesla Semi, Robotaxi launch, energy storage ramp). The broken promises cluster around the core operational metrics that actually drive shareholder value: profitability, cost reduction, margin protection, and volume growth.

The pattern is systematic: management promises "cost reductions and operational efficiencies" every year while margins compress every year. When results deteriorate, the narrative pivots — from "production growth" to "profitable growth" to "bringing artificial intelligence into the real world" [cred]. This is not strategy evolution; it is narrative evasion.

Specific commitments have vanished without acknowledgment: the Austin safety-driver removal target (set July 2025, missed, never mentioned again), the Cybercab April 2026 production start (flatly stated in January, silently missed by April), the year-end 2025 robotaxi coverage goal for half the U.S. population [cred]. When confronted with misses, management simply moves the goalpost further into the future.

The one-time tax benefit of $5.93B in FY2023 was allowed to dominate the narrative while the underlying operating decline was downplayed — a classic misdirection [cred]. External factors (tariffs, trade policy, supply chains) are cited as the cause of every miss, yet internal cost targets that management promised would offset these pressures consistently fail.

The CFO departures (Zachary Kirkhorn, August 2023) and the SVP Powertrain departure (April 2024, simultaneous with >10% headcount reduction) [er] add operational instability to a management team that is already credibility-impaired.

Bottom line on management: When management tells you they will deliver profitable growth and cost reductions, the historical record says the opposite will happen. Their forecasts on core automotive profitability have been consistently wrong in one direction — optimistic. A rational analyst must haircut any forward guidance from this team severely.

What the Numbers Tell Us About the Business

Tesla in 2026 is not a "wonderful compounder." It is not even a stable cyclical. The numbers describe a business whose core automotive franchise is undergoing a structural margin normalization — the slow, grinding process by which a once-differentiated product becomes a commodity.

Consider the evidence. Revenue is now shrinking in absolute terms [dp]. Operating margins, once the highest among volume automakers at 16.8%, have fallen to 4.6% — below what Toyota or Honda routinely deliver [pc]. ROIC of 4.8% barely exceeds the risk-free rate [pc], which means the business is destroying value on the margin. The moat that once existed — first-mover advantage in EVs, a superior charging network, manufacturing innovation — is being competed away as every major automaker now produces compelling electric vehicles.

The energy storage business (46.7 GWh deployed in FY2025) [10k-mda-2026-p1] is genuinely growing and genuinely promising. But it operates in a tariff-exposed environment that management itself warns about, and it is not yet large enough to offset the automotive decline.

What about Robotaxi, FSD, Optimus? These are the narratives the stock price lives on. But the numbers provide no basis to value them. There is no revenue line for Robotaxi. There is no segment disclosure for AI services. Management's own track record on autonomous driving timelines is, to put it charitably, disastrous. The Austin safety-driver promise, the Cybercab production date, the population-coverage targets — all missed without acknowledgment [cred].

This is why the circle-of-competence pre-screen flagged TSLA as "not understandable": the valuation hinges on "speculative autonomous driving and robotics initiatives with unpredictable cash flows and regulatory dependencies, making fundamental analysis unreliable" [pc-derived flag]. I agree. But even without relying on those flags, the existing business — the one with $94.8B in revenue and $4.4B in operating income — is worth perhaps $56/share on our DCF base case [pc]. In a 2008-replay scenario, it is worth $17.54 [pc]. In stagflation, $18.99 [pc]. The sensitivity grid shows that even with +10% growth and a 4-percentage-point margin improvement, the IV only reaches $53 [pc] — still 88% below the current price.

The gap between $56 and $429 is not a difference of opinion. It is the distance between a car company trading at a normal multiple of its deteriorating earnings and a quasi-religious belief that Tesla will achieve dominance in multiple trillion-dollar markets simultaneously. The numbers offer no support for the latter. The numbers actively contradict it.

Tesla at $428.96 is not an investment. It is a speculation on narratives that the historical financial record does not support, priced at levels that require growth beyond what any reasonable framework can justify.

Year-by-Year Specialist Reports

FY2021 — TSLA Specialist Report

Headline

FY2021 was the year Tesla’s manufacturing and delivery scale translated front-end revenue growth into an explosive step-change in profitability, cash generation, and balance-sheet strength. Revenue surged over 70%, but operating income multiplied more than fourfold, net income jumped nearly sevenfold, and free cash flow nearly doubled, all while the company halved its debt load. The numbers marked the clearest inflection yet from cash-burning growth to a self-funding, high-return industrial machine.

Numbers vs. Prior Year

Revenue: $53,823M, up 70.7% from $31,536M in FY2020. This was driven by record global deliveries of Model 3 and Model Y, after successful production ramps in Shanghai and Fremont, and the early output from the new Texas and Berlin factories.

Operating income: $6,523M, a 227.1% increase from $1,994M. Operating margin expanded from 6.3% to 12.1%, showing immense operating leverage as fixed costs were spread over much higher volumes and manufacturing efficiency improved.

Net income: $5,519M, up an astonishing 665.5% from $721M. This was not a tax-credit driven anomaly; the operating profit entirely reflected core business strength. The net margin rocketed from 2.3% to 10.3%.

Operating cash flow: $11,497M, up 93.5% from $5,943M. This was genuine cash conversion, not accounting noise, underscoring the quality of the income.

Capex: $6,482M, up 105.3% from $3,157M. The company doubled capex to fund new factories, cell production, and product development, yet still generated positive FCF. This is the hallmark of a business that can fund aggressive growth internally.

Free cash flow: $5,015M, an 80.0% increase from $2,786M. FCF after this investment boom indicates that Tesla no longer needed external capital to expand.

Owner earnings: $5,620M (including adjustments), a 679.5% leap from $721M, reflecting that even after accounting for maintenance needs, true economic earnings were enormous.

ROIC: 30.6%, up from 13.9%. This placed Tesla firmly in “wide-moat” territory for the year, signifying that reinvested capital was yielding returns far above its cost.

Total debt: $4,254M, down 49.7% from $8,462M. The company used its FCF to aggressively retire debt, deleveraging the balance sheet and reducing interest expense.

Cash & equivalents: $17,576M, down 9.3% from $19,384M. The decline is misleading—Tesla used cash to pay off debt and fund capex, yet still held a massive buffer.

Shares outstanding: 2,879.6M, a 429.3% increase from 544.0M. This jump is almost entirely due to the 5-for-1 stock split in August 2020 (year-end FY2020 shares likely reported pre-split, FY2021 post-split). Underlying dilution from stock-based compensation was modest relative to the shareholder value created, though SBC remains an ongoing cost.

What Management Said

The FY2021 10-K MD&A was not available for this analysis, so direct management commentary cannot be quoted. However, from contemporaneous quarterly letters and public statements, management consistently attributed the results to record deliveries, improved manufacturing cost per vehicle, scaling of higher-margin Model Y, and reduction in certain supply chain costs. CEO Elon Musk and CFO Zachary Kirkhorn frequently highlighted the “megacast” and structural battery pack as game-changers for margin expansion, and celebrated the achievement of industry-leading operating margins among volume manufacturers.

Numbers vs. Narrative

Even without verbatim MD&A, the gap between the typical narrative and the raw numbers is instructive. Management had long promised that growth would eventually produce GAAP profitability and robust cash flow; FY2021 delivered on that promise beyond any prior scale. Revenue growth of 70.7% outpaced most bullish forecasts, but the real surprise was the margin expansion: operating income grew 227%, far exceeding revenue growth, which points to genuine operating leverage rather than mere volume-add. The net income line (up 665.5%) suggests that prior years’ cumulative R&D and capex were now paying off with a steep drop in unit costs. If management emphasized “record” performance, the numbers fully vindicated that language. On the other hand, if the narrative downplayed the risk of share dilution, the data reveals that stock-based compensation continued—while the share count burst from the split, the underlying dilution rate must be monitored, as the multi-year trend warns that SBC averages 50% of reported FCF. FY2021’s owner earnings of $5,620M means that after SBC, true economic FCF would still be substantial, but it’s a caution.

Year-Specific Red Flags or Bright Spots

Bright spots:

- Operating margin crossed 12%, a level not seen in any prior year and historically rare for an automaker—this signaled that Tesla’s direct-sales model and low-cost manufacturing were structurally superior.

- Debt halved, eliminating any near-term solvency concerns and dramatically cutting interest costs.

- Free cash flow of $5B after doubling capex is a signal of “self-funding” hypergrowth; the company could now launch new products and factories without diluting equity.

- ROIC surged to 30.6%, a figure more typical of a software business than a capital-intensive manufacturer. This suggests the moat was real, at least temporarily.

Red flags:

- The share-count data shows a splitting effect, but the underlying increase from SBC must be separated. While the split is cosmetic, if the real share count rose even 5–10% from dilution, that would be a headwind for per-share value. The multi-year context notes that share-count dilution was +163.6% cumulative over the period (likely mixing pre- and post-split data), but for FY2021 alone, the jump is mechanical. It’s critical to distinguish genuine dilution from the split.

- Cash balance declined slightly while debt paydown consumed $4.2B; that was a wise allocation but it reduced liquidity, albeit from an extremely high level.

- The massive capex increase (+105%) may indicate that some of the margin and FCF strength was borrowed from underinvestment in prior years. If 2021’s capex needed to be sustained at these levels, future FCF might moderate.

What This Year Tells Us About the Trajectory

FY2021 was a definitive inflection year. After a decade of burning cash and funding growth with capital raises, Tesla demonstrated that its business model could generate sector-leading margins and returns on invested capital, self-fund an aggressive expansion, and rapidly deleverage. When interpreted in retrospect, a future analyst should see FY2021 as the year the “story” became a “financial reality.” It established that Tesla was not merely a top-line growth phenomenon but a legitimate industrial powerhouse capable of generating cash at scale. The key question left hanging was whether the margin expansion was sustainable or whether it reflected temporary factors (e.g., high-priced vehicle mix, pent-up demand, and limited competition) that would mean-revert as the EV market commoditized. The numbers give no definitive answer, but they set a high bar and a clear trajectory benchmark for subsequent years.

FY2022 — TSLA Specialist Report

Headline

FY2022 was the year Tesla’s financial engine roared to life with extraordinary force. Revenue crossed $81 billion, operating income more than doubled, and net income surged past $12.5 billion—all while the company nearly eliminated its long-term debt. The story of the year was one of unparalleled operating leverage: production volumes and vehicle deliveries grew, but margins expanded dramatically, proving that the manufacturing and pricing machine could produce not just cars but gushing cash flows. Beneath the headline numbers, however, decelerating revenue growth and persistent shareholder dilution signaled that the blistering pace of expansion was beginning to cool.

Numbers vs. Prior Year

Total revenue reached $81,462M, a 51.4% increase from $53,823M in FY2021. This was a strong absolute gain but represented a deceleration from the 71% growth rate of the prior year, hinting at maturing top-line momentum.

Operating income exploded 109.4% to $13,656M (from $6,523M), pushing the operating margin from 12.1% to 16.8%. This dramatic improvement reflected pricing power, manufacturing efficiencies, and fixed-cost leverage as production volumes ramped. Net income followed suit, soaring 127.5% to $12,556M (FY2021: $5,519M), translating into a net margin of 15.4%.

Cash generation remained robust: operating cash flow grew 28.1% to $14,724M (FY2021: $11,497M). Capital expenditures rose at a slower 10.4% pace to $7,158M (from $6,482M), yielding free cash flow of $7,566M, up 50.9%. Owner earnings, a measure of true economic profit after maintenance capex, nearly matched net income at $12,760M (up 127.0%), underscoring the quality of earnings.

The balance sheet transformed. Total debt plummeted 75.8% to just $1,029M (FY2021: $4,254M). Cash and equivalents dipped 7.5% to $16,253M, indicating that despite massive free cash flow, nearly all surplus was directed toward debt paydown—and likely other outflows—rather than cash accumulation. ROIC jumped from 30.6% to an all‑time high of 36.6%, reinforcing the year’s capital efficiency triumph.

The share count expanded 7.7% to 3,100.5 million, a continuing dilution pattern that quietly transferred value away from existing shareholders.

What Management Said

The MD&A provided for FY2022 (drawn from the year’s 10-K) focused heavily on the prior year’s achievements and set the tone for the ongoing ramp. Management highlighted that “we continue to ramp production, build new manufacturing capacity and expand our operations to enable increased deliveries and deployments” and pointed to the next phase of growth depending on “the testing and ramp at Gigafactory Berlin and Gigafactory Texas, as well as our ability to add to our available sources of battery cell supply by manufacturing our own cells.” They also acknowledged persistent industry‑wide semiconductor and component shortages, noting that “current production continues to be affected … requiring additional workaround manufacturing and production design solutions.”

The narrative emphasized production volumes and affordability as primary goals: “Our goals are to improve vehicle performance, decrease production costs and increase affordability.” There was little direct commentary in the outlook about the potential for record‑shattering profitability; instead, the focus remained on execution risks, supply‑chain constraints, and the capital‑intensive nature of the new factory ramps.

Numbers vs. Narrative

The management narrative’s cautious, production‑focused tone was overwhelmed by the numbers. While the MD&A underscored supply‑chain challenges and the difficulties of ramping new factories, operating margin increased by 470 basis points and net income more than doubled. The text’s language suggested that cost pressures were a headwind, yet the actual figures reveal an entity with remarkable pricing power and internal efficiencies that more than offset those pressures.

The debt paydown—a dramatic 75.8% reduction—received no explicit mention in the available narrative excerpts, even though it represented a strategic deleveraging of historic proportions. Management’s comment that “sustained growth has allowed our business to generally fund itself” understates the ferocity with which the balance sheet was restructured in FY2022. The numbers told a story of a company that, far from merely self‑funding its operations, was generating so much cash that it could retire virtually all its debt while simultaneously funding massive capital investments.

Where narrative and numbers align is in the production ramp: vehicle deliveries did indeed grow significantly in FY2022 (to roughly 1.3 million units), consistent with management’s focus on capacity expansion. However, the magnitude of profitability improvement—enabled by both volume and average selling price increases—was a story the narrative did not fully capture.

Year-Specific Red Flags or Bright Spots

The brightest spot was the combination of margin surge and debt elimination, which turned Tesla into a fortress of financial strength. ROIC at 36.6% represented a peak that future years would struggle to maintain.

Red flags are also specific to this year. The 7.7% rise in shares outstanding continued a long‑term pattern of dilution; stock‑based compensation remained a substantial hidden drag on per‑share value. The decline in cash (−7.5%) despite record free cash flow suggests that the debt paydown absorbed much of the surplus, and other investments or working‑capital drains may have further limited liquidity buildup. The deceleration in revenue growth from 71% to 51% marked the slowest pace in several years and foreshadowed the end of the extreme expansion phase. Additionally, the provided MD&A snippet lacks any mention of the China lockdowns that disrupted production in early 2022—probably because the text was truncated, but it is noteworthy that the full-year results overcame those disruptions so handily.

What This Year Tells Us About the Trajectory

FY2022 was an inflection year in which Tesla’s business model demonstrated its full profit‑generating potential. The dramatic margin expansion and debt paydown signaled maturation: the company was no longer a cash‑burning growth story but a cash‑gushing industrial powerhouse. However, the shrinking revenue growth rate and the persistent equity dilution pointed to a future where top‑line expansion would be harder‑won and where maintaining those peak margins would become the central challenge. Future analysts should view FY2022 as a high‑water mark for profitability and ROIC—a year that proved what the business could achieve under ideal pricing and demand conditions, but also one that set a very high bar for the years to come.

FY2023 — TSLA Specialist Report

Headline

FY2023 was the year Tesla’s growth came at a steep price—literally. While deliveries and revenue hit new records, a relentless price war gutted operating profitability: operating income fell 34.9%, free cash flow almost halved, and ROIC collapsed from 36.6% to 14.4%. A massive one‑time tax benefit of over $5 billion masked this erosion, pushing net income to an all‑time high and creating a deeply misleading headline. The year marked a fundamental shift from a high‑margin premium story to a volume‑at‑all‑costs model, with heavy capex for Cybertruck and new factories absorbing what little cash was left.

Numbers vs. Prior Year

(All figures in $M, except per‑share and ratios; YoY change in parentheses.)

| Metric | FY2022 | FY2023 | Change |

|---|---|---|---|

| Revenue | 81,462 | 96,773 | +18.8% |

| Operating income | 13,656 | 8,891 | –34.9% |

| Net income | 12,556 | 14,997 | +19.4% |

| Operating cash flow | 14,724 | 13,256 | –10.0% |

| Capex | 7,158 | 8,899 | +24.3% |

| Free cash flow | 7,566 | 4,357 | –42.4% |

| Owner earnings (net income) | 12,760 | 14,997 | +17.5% |

| ROIC | 36.6% | 14.4% | –22.2 pp |

| Operating margin | 16.8% | 9.2% | –7.6 pp |

| Total debt | 1,029 | 2,682 | +160.6% |

| Cash & equivalents | 16,253 | 16,398 | +0.9% |

| Diluted shares (M) | 3,100.5 | 3,164.1 | +2.1% |

- Revenue grew $15.3 billion to $96.8 billion, driven by higher deliveries, but the topline growth was aggressive price cuts that aimed to sustain volumes amid rising competition and softening demand.

- Operating income plunged $4.8 billion to $8.9 billion. The operating margin collapsed from 16.8% to 9.2%—a clear signal that cost reductions could not keep pace with the price cuts. This was the core deterioration of the year.

- Net income paradoxically rose to $15.0 billion, a $2.4 billion increase, entirely due to a non‑cash tax benefit of approximately $5.9 billion from the release of a valuation allowance on deferred tax assets. Without that one‑time item, pre‑tax income would have shown a significant drop.

- Operating cash flow fell $1.5 billion to $13.3 billion, despite the higher revenue, as working capital consumed more cash (likely inventory build) and margin compression reduced cash generation per vehicle.

- Capex surged $1.7 billion to $8.9 billion (+24.3%), the highest ever, reflecting the simultaneous ramp of Cybertruck, Tesla Semi, and factory expansions (Gigafactory Texas, Berlin). This is a tell‑tale sign of a company betting heavily on future volume.

- Free cash flow cratered to $4.4 billion, down 42.4%, as operating cash declined and capex soared. Real free cash flow after stock‑based compensation (which averaged ~50% of reported FCF across recent years) was even thinner.

- Owner earnings (net income) rose 17.5% to $15.0 billion, but this measure is distorted by the one‑time tax benefit; true economic earnings were far lower.

- ROIC nosedived from 36.6% to 14.4%, a staggering 22‑point erosion. This is the third consecutive year of decline and directly signals a deteriorating competitive moat.

- Debt more than doubled to $2.7 billion, though still modest relative to the cash pile. The increase likely reflects new financing for growth initiatives.

- Cash was essentially flat at $16.4 billion, as the combination of lower FCF and higher debt left the liquidity buffer unchanged. Share count continued to creep up (+2.1%), contributing to dilution that reduces per‑share intrinsic value over time.

What Management Said

Because the provided MD&A text corresponds to the FY2022 10‑K (the 10‑K filed in early 2023), it contains management’s forward‑looking narrative that set the stage for FY2023. Direct excerpts from that document—under “Management Opportunities, Challenges and Uncertainties and 2023 Outlook”—are highly instructive:

“We are focused on growing our manufacturing capacity… The next phase of production growth will depend on the ramp at Gigafactory Berlin‑Brandenburg and Gigafactory Texas, as well as our ability to add to our available sources of battery cell supply…”

“Our goals are to improve vehicle performance, decrease production costs and increase affordability.”

“Our cost reduction efforts, cost innovation strategies, and additional localized procurement and manufacturing are key to our vehicles’ affordability…”

“We will also continue to generate demand… by improving our vehicles’ performance and functionality… and delivering new vehicles, such as the Tesla Semi…”

“We continue to focus on improving our profitability through production and operational efficiencies.”

Management clearly telegraphed a strategy centered on volume growth, capacity expansion, and affordability. The emphasis on cost reduction and “improving our profitability” suggests they expected to offset price reductions with efficiency gains. The narrative painted a picture of controlled, profitable growth driven by manufacturing innovation.

Numbers vs. Narrative

The numbers tell a starkly different story than the confident tone of management’s outlook. While the narrative promised that cost innovations would protect profitability, the operating margin collapsed from 16.8% to 9.2%—a dramatic failure to translate cost reductions into margin preservation. The price cuts that made vehicles more “affordable” did stimulate revenue growth (+18.8%), but they came at the expense of operating income (–34.9%). The phrase “we continue to focus on improving our profitability” rings hollow when the actual operating profit dollars and margins both fell sharply.

The only reason net income rose was a one‑time tax benefit that management never highlighted in the outlook. Comparing the narrative’s “improving profitability” to the $4.8 billion operating income decline exposes a significant gap between rhetoric and results. The capex surge aligned with the narrative of “growing manufacturing capacity,” but the resulting free cash flow collapse—down 42.4%—was not foreshadowed as a near‑term risk. The narrative’s optimism about demand generation through new products (Cybertruck, Semi) did not mention that the contemporaneous aggressive pricing would gut margins far faster than new, higher‑margin products could compensate. In essence, management’s story of affordable growth neglected to warn that the price war would turn a high‑margin machine into a low‑margin volume play.

Year-Specific Red Flags or Bright Spots

- Bright Spot – Energy Storage and Solar Ramp: While not broken out in the provided slice, Tesla deployed record energy storage products and continued to scale its energy business, which will diversify revenue away from automotive.

- Bright Spot – Cybertruck and Semi Launch: Tooling for Cybertruck and pilot production of the Tesla Semi marked a genuine product expansion, fulfilling years of promises and potentially opening new high‑margin segments.

- Red Flag – Operating Margin Cliff: The 34.9% drop in operating income despite revenue growth is the single most alarming signal for moat stability.

- Red Flag – ROIC Implosion: Falling from 36.6% to 14.4% in one year, and now marking the third straight annual decline, suggests structural competitive pressures that management’s efficiency narrative could not overcome.

- Red Flag – Massive Tax Benefit Distortion: The $5.9 billion valuation allowance release obscured the underlying earnings decline; many analysts initially mistook the record net income as a sign of strength.

- Red Flag – Dilution & True FCF: Stock‑based compensation continued to consume a large share of reported free cash flow, meaning the true cash flow available to shareholders was significantly lower than the $4.4 billion headline. Shares outstanding inched up another 2.1%, adding to the cumulative dilution over time.

- Red Flag – Debt Spike: Debt jumped 160.6% to $2.7 billion, a notable increase that, while still low relative to cash, suggests Tesla may be financing growth with more leverage.

What This Year Tells Us About the Trajectory

FY2023 was an inflection year that shattered the high‑margin, high‑return model Tesla had enjoyed earlier in the decade. It demonstrated that price cuts as a volume lever are a double‑edged sword—they preserve demand but rapidly compress margins when the cost structure does not improve fast enough. The record net income was an accounting mirage; the underlying business became significantly less profitable and generated far less cash. For a future analyst, 2023 will serve as the year where Tesla traded its premium pricing power for volume and market share, putting its moat and returns on a downward slide. The heavy capex suggests the company is still betting on a future volume explosion, but the immediate evidence shows that growth is becoming increasingly capital‑intensive and less rewarding. In retrospect, 2023 will likely be seen as the year the narrative of ever‑improving profitability gave way to the reality of a commodity‑like, price‑sensitive transition.

FY2024 — TSLA Specialist Report

Headline

Fiscal 2024 was a year of strategic contradiction for Tesla. Revenue growth effectively stalled at just +0.9% despite significant capital expenditure (+27.5%), while operating income contracted by a fifth and net income was nearly halved—the latter primarily because the prior year’s massive one-time non-cash tax benefit did not repeat. The company ramped Cybertruck and poured cash into next-generation platforms, yet saw operating margins sink to 7.2% and free cash flow drop 17.8%. The year raises a critical question: is Tesla entering a prolonged investment phase where returns are deferred, or is the core automotive business losing pricing power and efficiency faster than new ventures can compensate? The surge in debt (more than doubling to $5.5B) and the flattish cash balance despite record operating cash flow suggest that capital intensity is rising just as earnings power softens.

Numbers vs. Prior Year

Revenue: $97,690M, up only $917M from $96,773M in FY2023 (+0.9%). Top-line growth essentially plateaued after years of rapid expansion (5-year CAGR +24.6%), signaling a sharp deceleration that far outstrips mere temporary slowdowns.

Operating income: $7,076M, down $1,815M (–20.4%). Operating leverage reversed dramatically; a mere 0.9% revenue increase accompanied a 20% profit drop, implying significant cost and price pressures. Operating margin contracted from 9.2% to 7.2%.

Net income: $7,091M, compared to $14,997M in FY2023 (–52.7%). The prior year’s figure included a $5.93B one-time non-cash tax benefit from valuation allowance release. Adjusting for that, FY2023 normalized net income would have been roughly $9.07B, making the FY2024 drop still a substantial 22% decline. The underlying earnings power deteriorated markedly.

Operating cash flow: $14,923M, up $1,667M (+12.6%)—a bright spot. OCF increased despite lower income, likely driven by working capital management or non-cash charges (e.g., depreciation from higher capex). This is a cash-generation highlight but should be probed for sustainability.

Capex: $11,342M, up $2,443M (+27.5%). Capital intensity surged as Tesla poured money into Cybertruck, next-gen platform, and factory upgrades. Capex as a percentage of revenue jumped from 9.2% to 11.6%.

Free cash flow: $3,581M, down $776M (–17.8%). FCF margin compressed to 3.7%. The cash left for shareholders after all investment shrank despite higher OCF, entirely because capex grew faster.

Owner earnings: For simplicity, we use net income as a proxy (no adjustment for maintenance capex given lack of disclosure), so $7,091M, down 52.7%. True owner earnings would likely be lower if we stripped out growth capex, but the direction is clear.

ROIC: 9.0%, down from 14.4%. This is a warning; ROIC has now declined for three consecutive years (from 36.6% peak), confirming moat erosion signals. The business is earning a lower return on invested capital even as it invests more.

Total debt: $5,535M, up $2,853M (+106.4%). Debt more than doubled, moving Tesla from a nearly debt-free posture to a meaningful levered position. While still manageable relative to equity, the rapid increase warrants attention, especially if rates remain elevated.

Cash & equivalents: $16,139M, down $259M (–1.6%). Despite generating $14.9B in OCF, cash barely budged, as capex and possibly debt repayments or share buybacks consumed the flow. The cash pile is large, but it is no longer growing.

What Management Said

Note: The MD&A text provided with this assignment corresponds to FY2023, not FY2024. A direct FY2024 10-K MD&A was not available for this specialist year dissection. Consequently, we reference the FY2023 management commentary to compare its forward-looking statements with what FY2024 numbers actually delivered.

In the FY2023 MD&A, management cited “total revenues of $96.77 billion, representing an increase of $15.31 billion” and emphasized “further cost reductions and operational efficiencies while maximizing delivery volumes.” They noted a focus on “ramping production, building new manufacturing capacity and expanding our operations to enable increased deliveries and deployments of our products,” and highlighted the Cybertruck as “Active” in production and the “Next Generation Platform” as “In development.” Management also warned that the next phase of growth would “depend on the continued ramp at our factories and the introduction of our next generation platform” and acknowledged “uncertainties inherent in establishing and ramping manufacturing operations.”

The FY2023 MD&A was aspirational about cost reduction and volume growth. The FY2024 actuals show that the revenue ramp stalled and cost efficiencies were insufficient to offset margin compression. Management’s 2023 narrative did not foreshadow a near-zero revenue growth year or a 20% operating income decline.

Numbers vs. Narrative

Where FY2023 management said, “we continue to ramp production... to enable increased deliveries... for further revenue growth,” FY2024 delivered revenue growth of less than 1%. The narrative of relentless volume expansion collided with reality. The MD&A’s language about “cost reduction efforts” and “operational efficiencies” sits awkwardly against a 20% drop in operating income on essentially flat sales.

Management in FY2023 mentioned a “one-time non-cash tax benefit of $5.93 billion” that inflated net income. The raw numbers for FY2024 show net income falling by over half, but once that benefit is backed out, the decline is still severe. The narrative in FY2023 would have implied that operational momentum was strong; the FY2024 numbers reveal that even normalized earnings power retreated.

The FY2023 MD&A’s discussion of “sustained growth” funding its own investments now looks stretched: FY2024 capex surged while FCF shrank, and debt doubled. The business did not self-fund its investment appetite this year—it leaned on new debt and consumed its prior cash flow.

Agreement exists only in the broad directional sense that Tesla did continue to invest heavily and launch new products (Cybertruck ramp). The MD&A’s caution about uncertainties in ramping new models proved prescient, but the magnitude of the growth stall and margin compression was not telegraphed.

Year-Specific Red Flags or Bright Spots

Red Flags:

- Revenue stagnation: 0.9% growth after years of 20-50% top-line expansion represents a dramatic deceleration that goes well beyond “pre-planned shutdowns” mentioned in the prior MD&A.

- Operating margin compression of 2.0 percentage points in a single year, pushing margins to 7.2%, the lowest in recent Tesla history, suggesting pricing pressure and/or cost overruns.

- Debt doubling to $5.5B: Tesla, long able to operate with minimal debt, suddenly levered up, possibly to fund capex without eating cash reserves.

- ROIC erosion continuing for a third year, now at 9.0%, which barely exceeds the cost of capital; signals that competitive advantages are weakening.

- Free cash flow after stock-based compensation: with SBC averaging 50% of reported FCF historically, true free cash flow available to equity holders is much smaller, and FY2024’s $3.58B FCF likely overstates economic reality.

Bright Spots:

- Operating cash flow hitting a record $14.9B, up 12.6% despite income decline, indicates strong cash conversion or favorable working capital shifts. This is a resilience signal.

- Cash & equivalents remain robust at $16.1B, providing ample runway for the heavy investment cycle.

- Capex surging to $11.3B signals serious commitment to next-generation products and capacity; if these bets pay off, they could reaccelerate growth later.

- Energy storage deployments (not detailed in the revenue mix but referenced in FY2023 MD&A context) may have contributed to revenue diversification, though their impact in FY2024 is unclear.

What This Year Tells Us About the Trajectory

FY2024 is a pivotal, potentially inflection year—but in a cautious way. After a decade of breakneck growth, the business hit a wall on the top line while ramping capital spending dramatically, compressing returns and forcing a debt-funded expansion. This looks less like a typical year and more like the opening act of a transition from a high-growth, capital-light (relatively) automaker to a capital-intensive, multi-product industrial company. Future analysts should view FY2024 as the moment when Tesla’s growth narrative decoupled from its financial reality; the company is now spending heavily to re-ignite growth, but there is no guarantee of success. The simultaneous margin erosion and investment surge could either set the stage for a new S-curve (Cybertruck, robotaxi, energy) or mark the beginning of a prolonged period of subpar returns. The red flags—especially ROIC decline and revenue stall—should be weighted heavily in any long-term valuation judgment.

FY2025 — TSLA Specialist Report

Headline

In FY2025, Tesla’s revenue engine stalled for the first time in years, and profitability cratered, but the company generated a surprise surge in free cash flow by slashing capital expenditures nearly 25%. The year was defined by a sharp divergence between operational momentum and cash generation—while vehicle deliveries, revenue, and margins contracted, management’s decision to dramatically cut investment spending temporarily juiced free cash flow, masking an underlying erosion of returns on capital and raising serious questions about the long-term growth trajectory.

Numbers vs. Prior Year

On a full-year fiscal basis, revenue fell 2.9% to $94,827M, the first annual top-line contraction since the Model 3 ramp era, signaling demand saturation and intensifying competition. Operating income dropped 38.5% to $4,355M, and net income attributable to common stockholders plunged 46.5% to $3,794M. That net income decline would have been even more severe if not for a $6.5B valuation allowance release that inflated FY2024’s baseline—adjusting for that, the underlying after-tax profit deterioration is even deeper. Operating cash flow held up surprisingly well, down only 1.2% to $14,747M, but the real story lies in capex: investment spending fell 24.8% to $8,527M, down from $11,342M. As a result, free cash flow (OCF less capex) soared 73.7% to $6,220M, a stark contrast to the crumbling income statement. Owner earnings, which we equate to net income, mirrored that 46.5% collapse. ROIC more than halved, from 9.0% to 4.8%, while the operating margin compressed from 7.2% to 4.6%, both well below the levels required to justify past capital intensity. Total debt ticked up 19.0% to $6,584M, though cash and equivalents edged 2.3% higher to $16,513M, leaving net cash largely unchanged. Shares outstanding increased 1.0%, a persistent but modest dilution.

What Management Said

The provided management commentary—extracted from Tesla’s FY2024 10-K, which was released in early FY2025—painted a bullish picture of the prior year and outlined a vision for continued expansion. Management highlighted 2024 total revenues of $97.69B, an increase of $917M YoY, and characterized the huge net income drop from 2023 as “primarily due to the impact of releasing $6.54 billion of our valuation allowance” in the prior year. They struck an optimistic tone about the future: “We are focused on profitable growth, including by leveraging existing factories and production lines to introduce new and more affordable products,” and emphasized “accelerat[ing] our AI, software, and fleet-based profits for further revenue growth.” Looking ahead, the narrative warned of potential near-term production disruptions from simultaneous manufacturing ramps of the New Model Y on three continents in Q1 2025, but maintained that “the next phase of production growth will depend on the continued ramp at our factories and be initiated by advances in autonomy and the introduction of new products.” There was no mention of an expectation of a revenue decline; instead, management signaled confidence that R&D and capital-intensive projects would drive the next leg of growth.

Numbers vs. Narrative

The actual FY2025 results brutally contradict management’s growth-oriented narrative. The MD&A’s emphasis on “profitable growth” and “further revenue growth” through AI, software, and fleet-based profits clashes with a 2.9% revenue decline and a 46.5% net income collapse. The declared focus on “leveraging existing factories and production lines to introduce new and more affordable products” appears to have produced affordability at the expense of margins, but not volume growth—unit deliveries likely fell or at best stagnated, as revenue contracted. Even more telling, the capex narrative completely unraveled: management’s 2024 letter had proudly noted $11.34B in capital expenditures, a $2.44B increase, and stated “we will continue investing in a number of capital-intensive projects and research and development in upcoming periods.” In reality, FY2025 capex shrank by $2.8B, an abrupt reversal that suggests either a chilling of the ambitious growth plans, severe cost cutting in response to competitive pressure, or a deliberate pivot to cash conservation. The resulting FCF spike—a 73.7% increase—was not driven by operational strength but by the deliberate suppression of investment spending. While management spoke of ramping new factories and vehicle models, the capex cut implies a deceleration of that very expansion, undermining the long-term growth narrative they were advancing just a year earlier.

Year-Specific Red Flags or Bright Spots

The most glaring warning signal is the FCF illusion: free cash flow improved from $3,581M to $6,220M, but only because capex was reduced by $2,815M—more than the entire $1,639M drop in operating cash flow. This is not a sign of business quality; it’s a result of pulling back the growth throttle. Worse, even after the cut, ROIC collapsed to 4.8%, suggesting the massive prior-year capex yielded little incremental profitability—a classic moat erosion symptom. Revenue declined for the first time in many years, breaking a decade-long growth trend, and the operating margin sank to 4.6%, far below auto industry leaders. Meanwhile, debt edged up to $6,584M while revenue shrank, nudging leverage higher. Another quiet red flag is the continuing share creep (+1.0%), which, when combined with the historical context that stock-based compensation has averaged 50% of reported FCF, implies that true free cash flow attributable to shareholders is significantly lower than the headline implies—once SBC is subtracted, real owner earnings are negligible. No large acquisitions or divestitures were noted, but the capex cut itself might hint at delayed or scaled-down projects, such as the next-generation vehicle platform, which management had previously touted as imminent.

What This Year Tells Us About the Trajectory

FY2025 stands as an inflection year—but a negative one. After years of hyperbolic growth, the business hit a wall in demand and pricing power, and the once-heralded investment cycle appears to have produced sharply diminishing returns. The decision to slash capex and boost FCF can be read either as a disciplined pivot to cash generation or as a loss of faith in future growth opportunities. The 4.8% ROIC, against a backdrop of still-substantial invested capital, signals that prior expansion has not created value. For a future analyst looking back, FY2025 will mark the moment when Tesla’s growth story gave way to a value mirage: free cash flow looked healthy, but the engine that produced it was one that was being starved of fuel. The year’s results strongly suggest the company had entered a phase of harvest, not build—a trajectory that, unless reversed by a genuinely transformational new product, points toward a low-return, mature industrial profile rather than the high-growth disruptor narrative of the past.

Recent Corporate Events

Recent Corporate Events — Multi-Year Pattern

Headline

Across FY2021–FY2025, Tesla executed a deliberate pivot from rapid operational expansion into a strategy centered on governance fortification and a new CEO compensation compact. The complete absence of M&A, the shift from a secured ABL to an unsecured $5.0 billion revolver, and the absence of any share repurchases or dividends reveal a firm conservatively husbanding liquidity. Simultaneously, the board has progressively hardened its defense against shareholder litigation—culminating in 2025 bylaw amendments that impose a jury trial waiver and a 3% ownership threshold to initiate derivative suits—while locking in Elon Musk’s incentives with a $23.7 billion interim restricted stock award and a new long-term performance award. This multi-year pattern reflects a Musk-centric, litigant-wary entity that is channeling resources into internal AI, energy, and manufacturing bets, deliberately avoiding external acquisitions and returning nothing to shareholders except dilution.

M&A Cadence

No acquisitions or divestitures were reported in any of the five fiscal years. Tesla did not pursue bolt-on acquisitions, transformative deals, or asset sales—an extreme outlier for a large-cap automaker or tech company. The entire growth strategy has been organic, relying on internal factory builds and product development.

Capital Allocation Arc

- 2022 (March–August): A 3-for-1 stock split in the form of a stock dividend. To enable the split, shareholders approved an increase of 4,000,000,000 authorized shares (votes: 815,392,835 for, 9,035,354 against). No new capital was raised; the split was purely a retail-share accessibility move.

- 2023 (January): Tesla entered into a $5.0 billion senior unsecured revolving credit facility with Citibank, N.A. as administrative agent, Deutsche Bank Securities Inc., and other lenders. The facility matures on January 20, 2028, carries variable interest (Term SOFR + 0.10% plus margin), and requires a $1.0 billion minimum liquidity. Simultaneously, Tesla terminated its existing asset-based revolving credit agreement with Deutsche Bank AG New York Branch; no borrowings were outstanding under either facility.

- 2025 (August, November): A massive equity-based compensation package. First, a special committee of independent directors (Robyn Denholm and Kathleen Wilson-Thompson) recommended and the Board approved the “2025 CEO Interim Award”: 96 million restricted shares to Elon Musk at a $23.34 per-share purchase price. The illustrative grant-date fair value was approximately $23.7 billion, though the company expects no compensation expense until the performance condition becomes probable. Subsequently, shareholders ratified the 2025 CEO Performance Award—a separate performance-based restricted stock award detailed in the September 17, 2025 proxy statement.

- Entire Period: No share repurchases, no dividends, and no public equity or debt offerings besides the undrawn revolver. The capital allocation framework is thus defined by extreme liquidity preservation combined with extraordinary potential dilution from CEO equity awards.

Strategic Investments / Stakes

No material equity investments, private-company funding rounds, or strategic stakes were disclosed across the five years. Tesla did not participate in any external venture funding (such as Anthropic rounds) and reported no minority investments.

Leadership & Governance Changes

- Departures: Jerome Guillen, President, Tesla Heavy Trucking (June 2021); Zachary Kirkhorn, CFO (effective August 4, 2023, succeeded by Vaibhav Taneja); Andrew Baglino, SVP Powertrain and Energy Engineering (April 2024), who left simultaneously with a >10% global headcount reduction.

- Board Appointments: Joseph Gebbia (September 2022, waived cash compensation); Jack Hartung (June 2025, appointed to Audit Committee, disclosed his son-in-law is a Tesla Service Technician earning ~$124,000).

- Governance Tightening: In April 2023, the board adopted proxy access (3% ownership for 3 years, up to 20% of board). In May 2025, bylaw amendments added a jury trial waiver for “internal entity claims,” imposed a 3% continuous ownership threshold for derivative proceedings, and clarified exclusive forum provisions. In September 2025, Tesla entered uniform indemnification agreements with all directors and executive officers, securing expense advancement and D&O insurance coverage under Texas law. The pattern is of an initially permissive governance structure progressively closing ranks—proxy access was introduced, but it was immediately followed by the sharp 2025 anti-litigation measures. Three senior operations leaders departed, with the CFO change being the most notable transition since 2019.

Regulatory / Litigation Trajectory

- 2021: Amendment #12 to the R&D Agreement with The Research Foundation for the State University of New York reset job and investment milestones at the Buffalo Gigafactory due to COVID-19 disruptions, managing a legacy SolarCity commitment.

- 2023: Settlement of the derivative action Police and Fire Retirement System of the City of Detroit v. Elon Musk, et al. in Delaware Chancery Court. A Stipulation of Settlement was entered on July 14, 2023, with a final hearing set for October 13, 2023.

- 2025: The bylaw amendments directly target future litigation risk, raising standing barriers. The 2025 CEO Interim Award explicitly includes an early forfeiture trigger if the final judgment in Tornetta v. Elon Musk makes the 2018 CEO Award fully exercisable—making the new grant a hedge against the litigation outcome. No material actions from the DOJ, FTC, SEC, or foreign regulators were reported. The trajectory shows settlement of a legacy derivative suit followed by preemptive, defensive bylaw rewrites.

POST-Latest-10-K Events (NOT in fundamental data yet)

None. The latest 10-K filed on February 1, 2026, encompasses all FY2025 events through the November 7, 2025 shareholder meeting. As of May 26, 2026, no subsequent 8-K filings have occurred. The $23.7 billion interim award, the 2025 CEO Performance Award vote, and the bylaw amendments were fully disclosed and debated months before the 10-K, and no new material events have emerged.

Pattern Risk Flags

- CEO-Centric Dilution Cascade: The $23.7 billion interim award, combined with the new performance award, sits atop the still-contested 2018 option. If all vest, dilution will be extreme, yet no expense is being recognized today—creating the risk of a sudden multi-billion-dollar catch-up charge that could devastate reported earnings.

- Litigation Defensive Overhaul: The simultaneous adoption of a jury waiver, a 3% derivative-suit standing threshold, and uniform indemnification agreements signals a board preparing for conflict with shareholders and insulating itself from accountability.

- Operational Churn: The departures of the CFO, the head of heavy trucking, and the powertrain SVP—coupled with a >10% workforce cut in 2024—raise questions about internal stability and growth trajectory.

- Zero M&A, Zero Capital Returns: In an industry where competitors consolidate and return capital, Tesla’s absolute refusal to acquire or reward shareholders directly—while issuing massive equity to the CEO—could reflect an insular, founder-controlled decision-making loop that disregards external capital discipline.

What’s Already Priced In vs What Isn’t

All major announcements—the interim award, bylaw amendments, shareholder votes, and the 2024 layoffs—are fully public and, given the many months since disclosure, have been absorbed into the stock price. The market has had ample opportunity to model the dilutive share count and the governance changes. What is not priced in is the timing and accounting impact of the $23.7 billion interim award expense. Because Tesla has deferred expense recognition pending performance-condition probability, a future sudden charge could meaningfully distort earnings in a single reporting period, surprising investors who treat the award as a non-event. Additionally, the 2025 bylaw provisions have not been tested in court; a judicial ruling striking down the jury waiver or 3% threshold—especially in the Tornetta context—could reintroduce litigation overhang that is currently discounted as stable governance.

Management Credibility

Year-by-Year Transitions

FY2022 → FY2023:

- Promised in FY2022 10‑K: “We are focused on increasing vehicle production, capacity and delivery capabilities… bringing new products to market” and explicitly cited the Tesla Semi as a new vehicle. → Actual FY2023: Deliveries grew 38% to 1.81M units. New product: Tesla Semi entered pilot production. kept

- Promised in FY2022 10‑K: “Our goals are to improve vehicle performance, decrease production costs and increase affordability.” The outlook discussed cost‑reduction efforts as the mechanism for affordability, implying stable margins. → Actual FY2023: Significant price cuts made vehicles more affordable, but cost reductions could not keep pace: operating income fell 34.9% (to $8.89B), operating margin contracted from 16.8% to 9.2%. Affordability rose, but the implicit promise of margin‑protected growth was not kept. partial (affordability achieved, cost‑reduction and profitability promise broken)

- Promised in FY2022 10‑K, via the ongoing narrative: “We continue to focus on improving our profitability through production and operational efficiencies.” → Actual FY2023: Operating income declined $4.8B. Net income rose only because of a $5.93B non‑cash tax benefit; underlying pre‑tax earnings fell sharply. broken

- Promised in FY2022 10‑K: “The next phase of production growth will depend on the ramp at Gigafactory Berlin‑Brandenburg and Gigafactory Texas.” → Actual FY2023: Both factories ramped, contributing to the delivery increase. kept

- Promised in FY2022 10‑K: Battery cell supply growth through “manufacturing our own cells.” → Actual FY2023: 4680 cell production was still ramping, no material shift in supply mix reported. unverifiable

FY2023 → FY2024:

- Promised in FY2023 10‑K: “We continue to focus on further cost reductions and operational efficiencies while maximizing delivery volumes.” → Actual FY2024: Deliveries fell to 1.79M (‑1.1% YoY). Operating margin sank further to 7.2% (from 9.2%). Cost reductions did not prevent margin erosion. broken

- Promised in FY2023 10‑K: “Delivering new vehicles, such as the Cybertruck and next generation platform.” → Actual FY2024: Cybertruck moved from tooling to active production; deliveries began. Next‑generation platform remained “In development.” kept (Cybertruck)

- Promised in FY2023 10‑K: “The next phase of production growth will depend on the continued ramp at our factories.” → Actual FY2024: Factory ramps did not translate into volume growth; total production was essentially flat. broken

- Promised in FY2023 10‑K: Ongoing focus on “improve vehicle performance, decrease production costs and increase affordability.” → Actual FY2024: Revenue grew only 0.9% despite aggressive pricing; affordability was maintained but with further margin compression. Operating income fell 20.4%. broken (profitability deteriorated)

FY2024 → FY2025:

- Promised in FY2024 10‑K: “We are focused on profitable growth” and “increasing vehicle production, utilized capacity and delivery capabilities.” → Actual FY2025: Revenue fell 2.9% (to $94.8B), deliveries declined to 1.64M units. Operating income collapsed 38.5% to $4.36B, net income nearly halved to $3.79B. broken

- Promised in FY2024 10‑K: “Reducing costs” and “further cost reductions and operational efficiencies.” → Actual FY2025: Operating margin compressed to 4.6% (from 7.2%), the lowest in the period. Margin compression accelerated, showing cost reductions were insufficient or offset by price cuts. broken

- Promised in FY2024 10‑K: “Ramping the production and increasing the market penetration of our energy storage products.” → Actual FY2025: Energy storage deployments surged to 46.7 GWh (+49%). kept

- Promised in FY2024 10‑K: “Further improving and deploying our FSD (Supervised) capabilities, including future autonomous capabilities through our purpose‑built Robotaxi product, Cybercab.” → Actual FY2025: Robotaxi service launched in June 2025. kept

- Promised in FY2024 10‑K: Battery and AI compute technology development; “vertically integrating and localizing our supply chain.” → Unclear measurable progress by year‑end 2025. unverifiable

Pattern Observed

Aggregate count: 7 kept · 1 partial · 7 broken · 3 unverifiable across 3 transitions.

Management consistently over‑promises on core automotive growth and margin improvement while delivering on new product launches and energy storage. The operating narrative (“cost reductions,” “production efficiencies”) is repeated even as margins decline year after year, indicating a systematic optimism bias. When results deteriorate, the outlook pivots toward new technology narratives (FSD, Robotaxi, AI) rather than candidly addressing the structural margin compression in the legacy auto business.

Language Evolution

- From “production growth” to “profitable growth”: FY2022 MD&A emphasized “ramping all… vehicles to their installed production capacities.” By FY2024 MD&A the phrase “profitable growth” appeared, trying to signal discipline, yet actual profitability cratered in FY2025.

- Rise of AI/Robotaxi language: FY2023 MD&A still focused on “vehicles, battery technologies, FSD.” FY2024 MD&A introduced “purpose‑built Robotaxi product, Cybercab” and “accelerate our AI, software, and fleet‑based profits.” FY2025 MD&A (FY2026 10‑K) opened with “We are focused on bringing artificial intelligence into the real world,” demoting the automotive mission. This shift suggests management redirects narrative away from the stalling core auto business.

- Disappearing “cost reduction” credibility: “Cost reduction efforts” and “operational efficiencies” were frequently used, but after FY2023’s operating margin implosion, the terms lost conviction; by FY2025, they were hollow mentions amid continued margin decline.

- Tone shift: The FY2022 and FY2023 MD&A were upbeat about volume ramp and efficiency; the FY2024 MD&A, while still optimistic, inserted cautious language about “uncertainties inherent in establishing and ramping manufacturing operations.” By the FY2025 MD&A (for 2025), language turned defensive: “rapidly evolving trade and fiscal policy, uncertainty… risks to our global supply chain… could have a meaningfully adverse impact.” The tone moved from confident to blame‑the‑environment.

Specific Kept Promises (credibility deposits)

- Tesla Semi pilot production: Teased in FY2022 MD&A as an upcoming new vehicle; pilot production began in FY2023 at Gigafactory Nevada. Kept.

- Cybertruck launch: Described as “Tooling” in FY2022, “Active” in the FY2023 outlook; deliveries started in FY2024. Kept, albeit years later than originally promised, but within the explicit forward‑looking window.

- Energy storage ramp: Promised in FY2024 MD&A to ramp production and market penetration; storage deployments leaped from 31.4 GWh in 2024 to 46.7 GWh in 2025 (+49%). Kept.

- Factory ramps (Berlin / Texas): Both factories were active and contributed to the FY2023 delivery jump from 1.31M to 1.81M units, fulfilling the FY2022 promise. Kept.

- Robotaxi service launch: Although not given a specific date in FY2024 MD&A, the focus on Cybercab and autonomous capabilities culminated in a June 2025 launch. Kept.

Specific Broken Promises (credibility withdrawals)

- Profitability improvement (FY2022→2023): The narrative of “improving our profitability” was contradicted by a 34.9% operating income decline, from $13.66B to $8.89B. The only reason net income rose was a $5.93B one‑time tax benefit. Broken.

- Cost reductions protecting margins (FY2023→2024): Despite stating “further cost reductions and operational efficiencies,” operating margin fell to 7.2% (‑2.0pp). Delivery volumes slightly declined, showing cost cuts did not keep pace with price competition. Broken.

- Revenue and volume growth (FY2023→2024): Management highlighted “maximizing delivery volumes” and factory ramps, yet deliveries decreased 1.1% and revenue advanced only 0.9%. The expectation of continued growth was unmet. Broken.

- “Profitable growth” and “increasing vehicle production” (FY2024→2025): FY2024 MD&A’s explicit emphasis on profitable growth failed spectacularly: revenue down 2.9%, deliveries down 8.4%, net income down 46.5%. The promised increase in vehicle production turned into a steep decline. Broken.

- Cost reduction delivering margin improvement (FY2024→2025): Again, with “further cost reductions and operational efficiencies,” operating margin fell further to 4.6%, the lowest of the period, signaling that either cost reductions were insufficient or pricing pressure overwhelmed them. Broken.

Spin & Euphemism Patterns

- “Affordability” as a shield for margin erosion: In FY2022 and FY2023 MD&A, “increase affordability” was presented as a goal achieved through cost innovation; in reality, it was executed through massive price cuts that decimated margins. The phrase obscures the trade‑off.

- “Challenging environment” / external scapegoating: When results weakened, management increasingly cited external factors: “industry‑wide component constraints” (FY2022), later “rapidly evolving trade and fiscal policy, uncertainty… tariff regime” (FY2025). These are used to deflect from the failure of internal cost targets.

- “Investing for the future” / “capital‑intensive projects”: The company justified rising capex and falling FCF with this language, but in FY2025, when it cut capex by 24.8% to boost FCF, the narrative did not acknowledge the retreat. This inconsistency makes the “investing” mantra a convenient pivot.

- One‑time tax benefit distortion: In FY2023, net income hit a record, but management’s commentary only briefly noted the $5.93B tax benefit. The strong income figure was allowed to dominate the narrative while the severe operating decline was under‑emphasized, a classic misdirection.

- Narrative rebranding: As auto margins crumbled, the MD&A shifted focus from automotive production growth to “AI, software, and fleet‑based profits” and then to “bringing artificial intelligence into the real world.” This evolution looks less like genuine strategy change and more like re‑framing the story to distract from a deteriorating core business.

Credibility Grade (A–F)

D